Coffee Industry in China

1. Overall fast-growing Chinese coffee industry

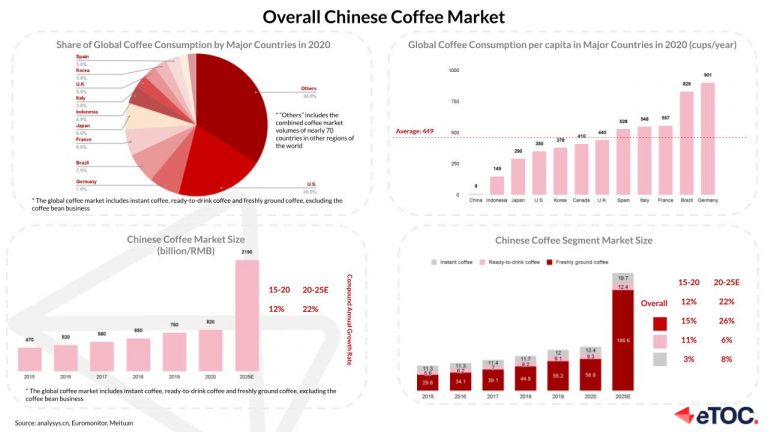

According to analysys.cn, for the global coffee market, Europe, America, Japan and South America are relatively well developed, with China accounting for only 2% of coffee consumption in FY2020, and per capita consumption far lower than in other mature coffee markets.

However, China’s coffee market is growing rapidly, with a CAGR of 22% over 2020-2025, reaching RMB 219 billion in 2025. Cumulative investment in China’s coffee industry reached 18 times by October 2021, with a cumulative investment of 5.69 billion yuan based on iimedia.cn. Local brands are powering up and growing, with eight investments between June and July of 2021.

Generally, coffee products fall into four categories.

- Coffee beans: priced 6-100 RMB/100g

- Instant coffee: including coffee concentrates, drip bag coffee, coffee capsules, instant coffee powder, etc.

- Ready-to-drink coffee: a cold drink that comes pre-made in a can or a bottle, priced at 5-20 RMB per bottle

- Freshly ground coffee: mainly found in coffee shops, convenience stores and restaurant brands, priced at 10-50 RMB per cup

The Chinese coffee market referred to in this article does not include the coffee bean business. Based on analysis.cn, freshly ground coffee is the most prominent performer in the coffee industry, with an expected CAGR of over 25% in the next five years and a market size of over RMB180 billion in 2025.

2. The current state of coffee consumption in China

2.1 Who are the Chinese coffee consumers

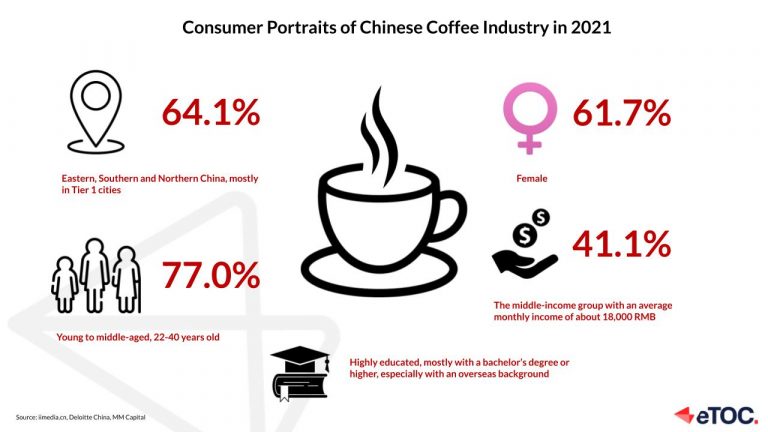

According to iimedia.cn, Chinese coffee consumers in 2021 are mainly concentrated in Eastern, Southern and Northern China, predominantly female, 22-40 years old and of medium income. According to Deloitte China & MM Capital, the higher the consumer’s income and the longer they have been drinking, the more frequent coffee intake.

2.2 How do Chinese consumers consume coffee

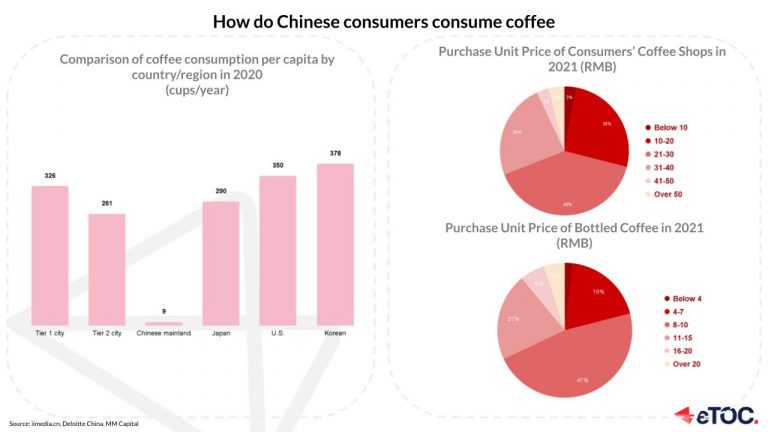

For the frequency, there are significant differences between cities based on Deloitte China & MM Capital, consumers in Tier 1 and Tier 2 cities are comparable in consumption to mature markets such as Japan and the United States. In particular, coffee consumption in Tier 1 cities per capita reached 326 cups/per year.

Regarding the price, Chinese consumers spend between RMB 10-40 for a cup of fresh ground coffee in a coffee shop and between RMB 4-15 for a bottled ready-to-drink coffee.

2.3 Why Chinese consumers consume coffee

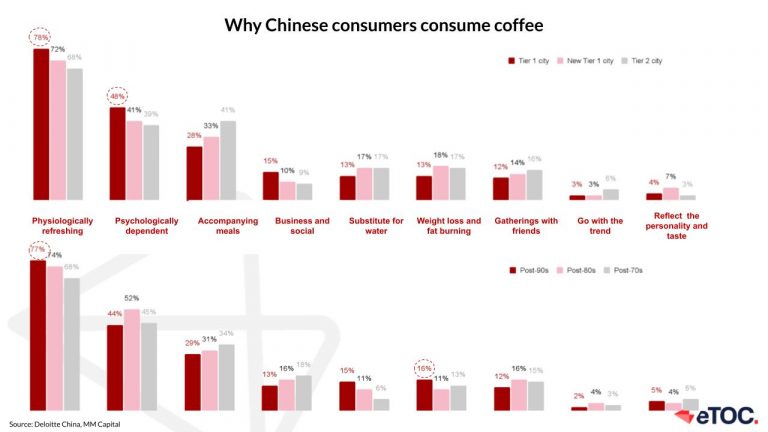

Based on iimedia.cn, people consume coffee for two main reasons: to Consumers consume coffee for two main reasons: to refresh themselves (53.1%) and to enjoy the taste of coffee (52.2%), but also because they enjoy the atmosphere and service of the coffee shop (31.3%), social needs (22.4%), etc.

In the case of freshly ground coffee, it is more of a functional need to satisfy a physical and psychological dependency. Deloitte China & MM Capital has also observed that coffee intake for the purpose of weight loss and fat burning is on the rise among young people due to health consciousness.

3. Three main trends in the coffee industry to keep an eye on in 2023

3.1 Fiercer competition

- More entry brands: The coffee industry remained to be investors’ preference. In 2022H1, there were 14 coffee events with a total value of ¥1.8 billion. Among them, Tims, Seesaw and Coffee Wings are all over ¥100 million. New entrants include cross-border brands (e.g. China post, Huawei), new tea brands (e.g. LELECHA, Cha Yan Yue Se).

- Online and offline competition: Online brands (such as Saturnbird, Yongpu) opened offline stores; offline stores (such as Luckin coffee, Starbucks) also accelerated their layout online, selling coffee beans, peripheral products, etc.

3.2 Sinking market

As in Tier 1 & 2 cities, the average consumption of coffee per capita is 326 and 261 cups per year, with consumption levels close to mature markets. The competition is fierce so coffee brands are turning to the sinking market

- Coffee chain brands: The first coffee chain brand to focus on the sinking market is Lucky Cup(幸运咖). For now, the brand stores have reached 1,805 with 50% of the stores in Tier 3 & 4 cities and below. The same strategy has been adopted by international brands. Starbucks has announced it will reach 9,000 total stores by 2025, doubling its net revenue and targeting more Tier 3 & 4 markets.

- Independent cafe: According to Xiaohongshu, young people return to their hometowns to start their own businesses, with 45% choosing to start with food & beverage. 35% of the Xiaohongshu “cafe startups” in 2021 came from Tier 3 cities and below.

3.3 Quality upgrading

- Specialty instant coffee continues to capture share: Although the growth rate of instant coffee as a whole is slowing down, the specialty instant coffee is growing rapidly, ranking first in the coffee industry for two consecutive years. In the 2022 Tmall Double 11 coffee cereal soluble powder category, 4 out of 10 are specialty instant products.

- Craft upgrade: Instant coffee coincidentally highlights its grinding and extraction process, reflecting better taste and quality, such as the micro-grind process, which can keep the original taste of coffee

- Origin preference expansion: China is growing significantly as an up-and-coming origin. Yunnan is the largest domestic coffee bean producer, extending towards boutique and deep processing.

4. Key Takeaways of Chinese coffee market

Overall, the Chinese coffee market is still in a phase of rapid development and the competition is fiercer regarding the brand numbers and channels. Tier 1 & 2 coffee markets are close to a mature market so brands are exploring the sinking market and upgrading coffee quality. Among all coffee, freshly ground coffee grows at the most pronounced rate, demonstrating consumers’ need for high-quality coffee. Brands are upgrading the coffee quality, such as a new sub-category (specialty instant coffee), crafts, and origins.

Coffee consumers are mainly aged 22-40, with a medium income and a high level of education. The main reasons for drinking coffee are physiological and psychological needs or love of coffee taste. With coffee becoming more popular in China, consumers will further diversify.